A finance lead I spoke with recently described her morning. She logs into one bank to check GBP balances, a second portal for EUR, an FX provider for AED, a custody dashboard for stablecoins, and a block explorer to confirm an on-chain transfer that left the building the day before. By the time she's answered "is this paid?" for any single transaction, she's opened five tabs and reconciled three different identifiers in her head.

That picture isn't unusual; it's the default. For most of the last decade, fiat payments and crypto payments have been built and bought as completely separate systems - separate vendors, separate ledgers, separate compliance stacks, often separate teams. That worked when stablecoins were a curiosity, but stops working the moment those assets become integral to customers' needs.

The cost of parallel universes

When crypto sits in a different system from fiat, the seams show up in the customer's books. They show up as a month-end close that takes three days instead of three hours. They show up as a treasury question (how much liquidity do we actually have, right now?) that nobody can answer on a single screen. They show up as duplicate onboarding, where the same customer verifies themselves twice because two systems don't share a customer model. They show up at audit time, when no single trail of activity exists for any one counterparty.

Independent analysis now puts B2B stablecoin payments at around $226 billion for 2025, with B2B accounting for roughly 60% of all stablecoin payment volume. That's no longer experimental; it's a critical flow. And in most platforms, it's flow that has been bolted onto a system that wasn't designed for it.

What unified rails actually means

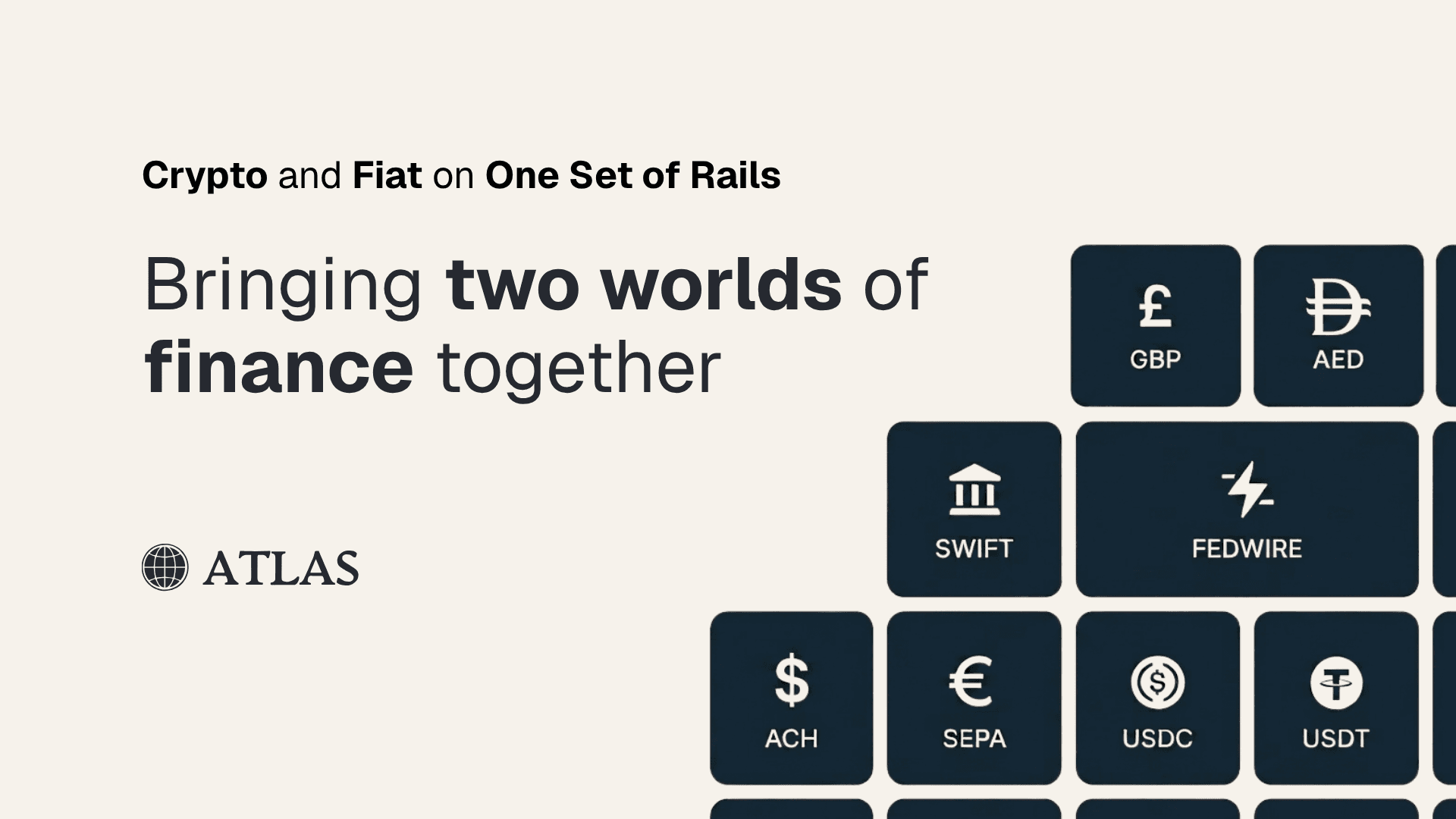

A unified rails platform treats every movement of money the same way at the layer the customer cares about. One instruction. One vocabulary for status. One activity view that combines fiat and crypto in a single list. The rail used is secondary.

The underlying principle is simple: crypto is just another rail. Same workflow, same flexible permissions, and same people. The novelty of the asset class is contained in the detail; the discipline at the centre is the same as any well-run payments business.

It helps to separate two things that often get conflated. The customer's intent - "move this much from here to there, in this currency, by this time" - is rail-agnostic. It belongs at the top of the platform. The execution of that intent (which network, which provider, which confirmation mechanism) is rail-specific. When those two layers are fused together, the customer ends up reasoning about wallets, chains and partner clearing windows just to send a payment. When they're cleanly separated, the customer describes an outcome and the platform handles the rest.

What this looks like in practice

Single instruction model: From the customer's perspective, it is one payment. From the platform's perspective, it is one record with a structured execution graph. The benefit is that the customer's reporting, dashboards and workflow don't break when a transaction happens to use crypto rails.

Unified activity view across rails: Every account a customer holds, fiat or crypto, appears in the same place, and every transaction across those accounts appears in a single combined list. The customer never has to leave the platform to assemble a picture of their activity. "Where is this payment right now?" becomes a question with one answer on one screen, rather than a five-tab investigation.

Consistent vocabulary for status: There's a small, deliberate set of states applied to every payment, regardless of rail. A finance team should never have to learn one set of terms for SEPA returns and another for block-confirmation thresholds. The rail-specific confirmation logic stays under the surface; the status that surfaces is the status that matters.

Live updates driven by the payment rail: The platform doesn't wait for nightly batches to discover that something happened, it reflects what the rails say as the rails say it. When something goes wrong, the error is visible in the customer's view, not buried in someone else's exception queue. Operations teams help triage where they need to, but the customer is never the last to know about their own payment. That is what real-time means in payments: not artificially fast, but honestly current.

Why this argument is a 2026 argument

The reason this is worth writing about now, rather than in five years, is that two regulatory deadlines are forcing the question, and one market trend is making it material.

In the UK, the Financial Conduct Authority's supplementary safeguarding regime, the new CASS 15 sourcebook for payments and e-money firms, comes into force on 7 May 2026. It mandates daily reconciliation against safeguarded funds, monthly returns to the regulator, an annual safeguarding audit, and a maintained resolution pack. Firms that already operate with a single, disciplined view of customer activity across rails will treat this as a tightening of existing practice. Firms that don't will be re-architecting under deadline pressure.

In the EU, the Markets in Crypto-Assets Regulation reaches full application by 1 July 2026, with stablecoin-specific provisions already live and crypto-asset service providers required to be authorised across the bloc. MiCA does not accept "we run two parallel systems" as a compliance posture. It expects a single, coherent record of customer activity, transferable identity, and unified transaction monitoring.

Underneath both is the simple market reality. The Financial Stability Board's October 2025 thematic review flagged fragmented and inconsistent oversight as the largest standing risk in the global crypto regime. The customers being onboarded today expect crypto and fiat as a single product, not two products with a shared logo.

What good actually means

A platform that does this well is not impressive because it supports more payment types. It's valuable because the customer's finance, operations, treasury and audit functions don't have to fork by asset class. One instruction. One vocabulary. One activity view. The rails underneath can change as fast as the world does, new currencies, new networks, new compliance regimes and the customer never has to. That is what "future-proof payments" actually means.

The five-tab morning is not a problem of technology. It's a problem of where somebody drew a line. Drawing it in the right place, between the customer's intent and the rail that carries it is the whole game.

Learn More

As global finance increasingly converges around unified fiat and digital asset infrastructure, operational simplicity is becoming a competitive advantage for modern businesses and institutions.

Atlas Financial enables professional clients to manage fiat payments, digital assets, treasury operations, and settlement infrastructure within a single operational environment designed for modern financial workflows.

Explore how Atlas supports Banking & Custody, On & Off Ramping, Yield, and Staking solutions through institutional-grade infrastructure built for global financial operations.

Access the demo or schedule a conversation with our team: https://atlas.financial/?modal=interactive-demo

You can also discover how Atlas supports institutional On & Off Ramping and multi-rail payment infrastructure for modern treasury and operational finance teams.

Learn more about Atlas On and Off Ramping solutions: https://atlas.financial/on-off-ramping